When you think of cooking up salsa, what’s the first thing that comes to mind? Tomatoes. But you know that’s not it. You’ll need onions, jalapenos, cilantro, garlic and a few more things. You mix all that in the right proportion and you’ve got your salsa.

Craig L. Israelsen, professor of all things financial planning at the Brigham Young University likens the art of portfolio construction to making salsa. I mean you can add your own flavor to a recipe but ultimately, the ingredients that constitute a wholesome salsa don’t differ much. And so shouldn’t the ingredients of your portfolio.

The recipe is your portfolio’s asset allocation. There are complex elements to it but inherently, not that complex.

Some of the elements that make up a salsa, say salt for example, may not be very exciting. And they are not supposed to be. They are neutralizers.

A well-designed portfolio should have its own set of neutralizers.

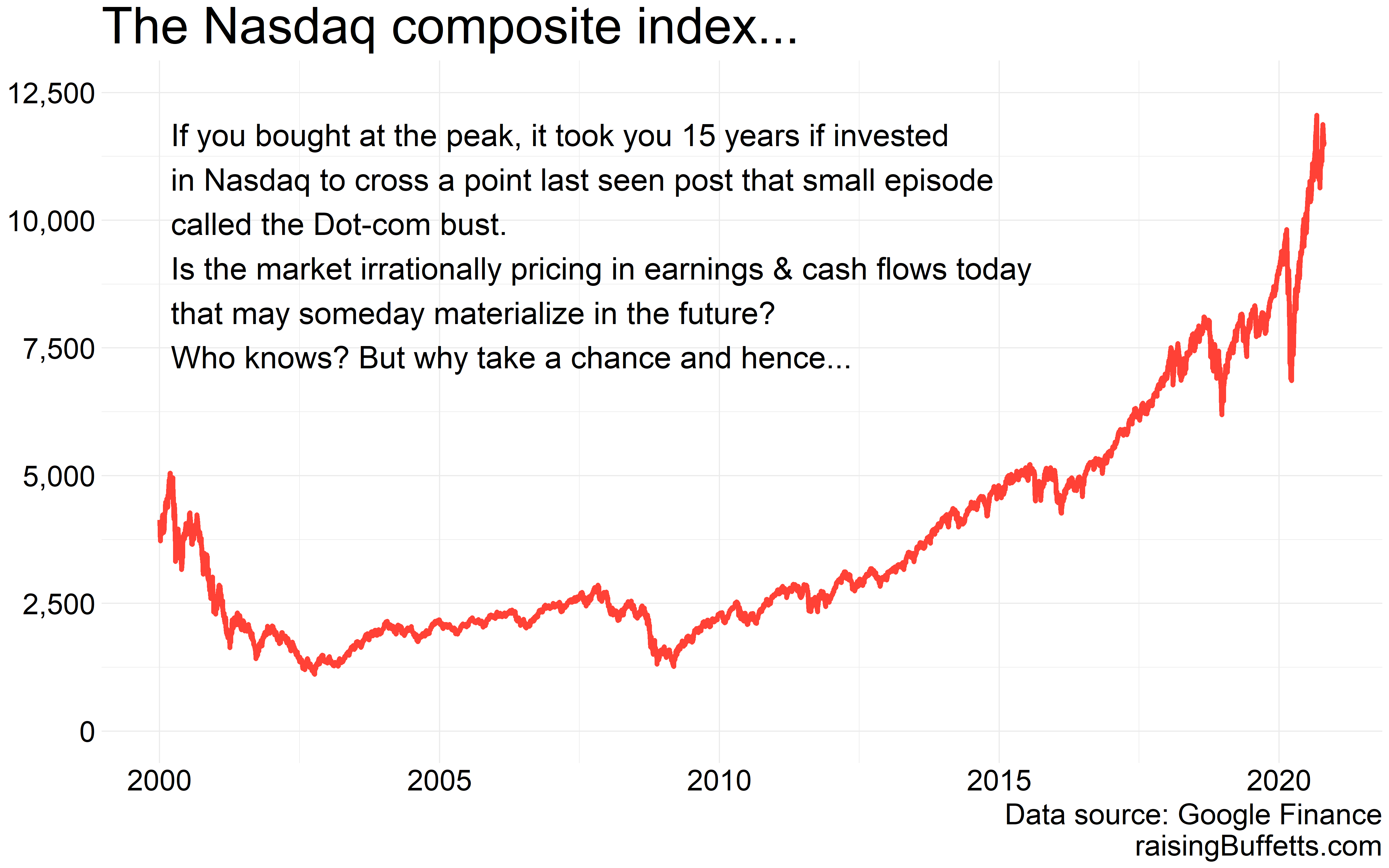

But then we’ve got a world where the only thing that matters is how you compare against the S&P 500 index. At least lately. Or God forbid, the Nasdaq. Talking about Nasdaq…

Comparisons against these indices didn’t happen as much during the decade of the 2000s when indices similar to these sucked wind but they happen now because we forget. We are too busy. We take mental shortcuts instead of thinking deeply about what we own and why.

And since when do we compare salsa to 500 ground-up tomatoes? We have created a misconception around what diversification is. The S&P 500 is a diversified set within an asset class. That’s not true diversification. That’s intra-diversification. It’s depth, not breadth.

And Nasdaq’s worse. Yes, yes, a lot of companies that make up that index will go on to change our world but it’s still mostly a narrow subset of the investible universe. And there are other means to own it.

So getting both breadth and depth is true diversification. A multi-asset portfolio that encompasses a need appropriate allocation is what you want.

A 60-year old’s portfolio should look different than that of a 30-year old.

A 60-year old’s portfolio with a solid pension should also look different than that of a 60-year old’s without a pension.

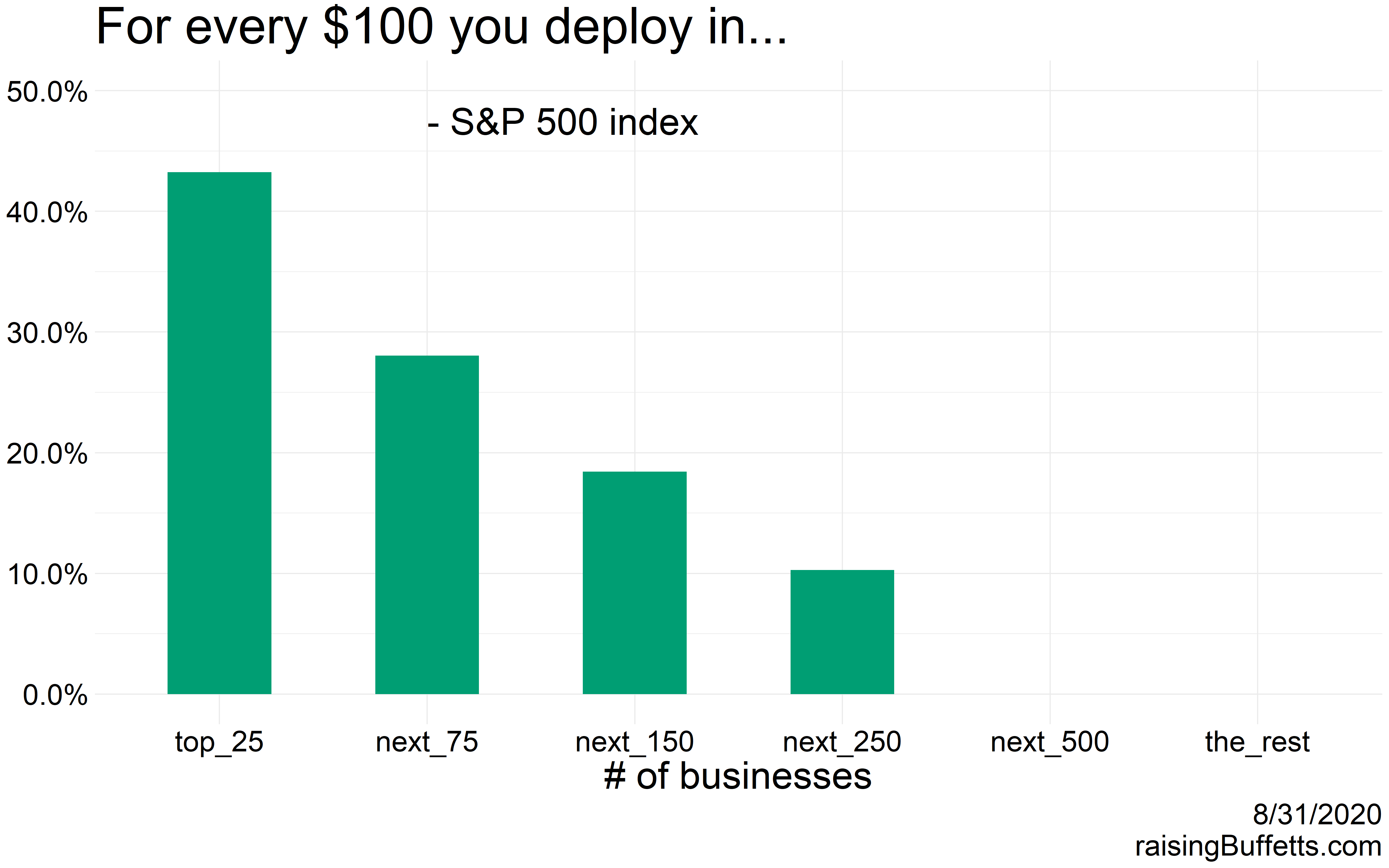

Back to the S&P 500, this is what you get when you own just it.

So the biggest 25 businesses take up almost 45% of your money. Even in a winner take all kind of an economy, that’s too much concentration in just a few businesses if this is all you’ll do with your money.

And large businesses don’t stay large forever. They become stodgy, bureaucratic and unmanageable and eventually get replaced by smaller, more nimble rivals. It is only a rare breed that can maintain their market power for decades on. A prime example of that process and there are many is General Electric which at one point was the largest market value business in the world but now is a shell of its former self.

The current bunch of the large cap universe could be an exception but history says otherwise. There is always something around the corner that would dislodge the hot ones of today. It might take longer but it’s going to happen.

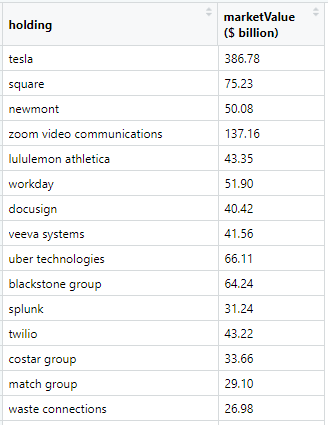

Plus a portfolio invested only in the S&P 500 index leaves out stalwarts like these and 3,000+ others…

Not a collection that screams of deep value but it is a collection.

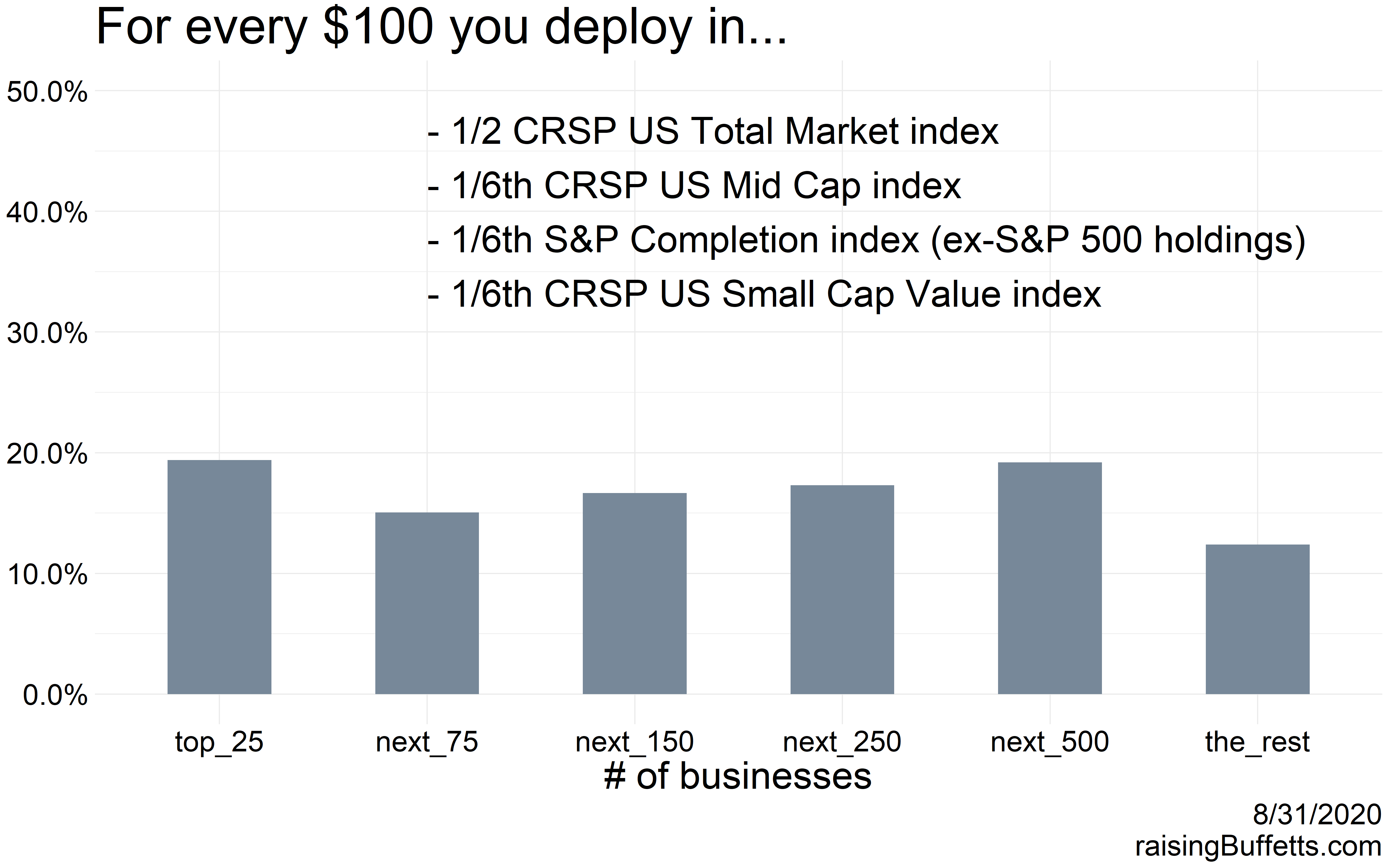

So what’s a flavor of depth and breadth? Maybe this…

That’s for domestic equities. The ingredients and the proportions can change based on where you are in life but seems even-keeled and at least pointing in the right direction. You do something similar for international equities. Then you bring in bonds and cash, real estate and alternatives. Now that’s salsa.

On bonds, the last 40 years have been the best 40 years in the history of the fixed-income world. That’s not going to be repeated so caution on what type and duration to own is warranted.

And the portfolio you design should be a function of how much you’ve saved, what you’ll continue to save plus growth in value. Expecting just your portfolio to do the heavy-lifting without a pitch from your savings is not going to cut it in this yield-starved world. Encounter anything that promises that, run.

And last, as Carl Richards, the author of The Behavior Gap says, you can have the best portfolio ever designed in the history of the world and you make one behavioral mistake a decade, you might as well have stuffed all that cash in a mattress.

So don’t.

Thank you for reading.

Until later.

Cover image credit – Karolina Grabowska, Pexels