Finance theory tells us that in order to eliminate any company specific risk, all you need to own is a basket of stocks in 20 to 30 companies representing a broad spectrum of an economy. That is what the Dow Jones Industrial Average with its 30 components does by acting as a barometer for the U.S. economy. And it’s done a fairly decent job at doing just that.

So that’s for the U.S. Then you do the same for the international stock markets and then the bond markets to some extent and so on.

But in this day and age where a company or an industry can be disrupted out of existence in time-frames that are much shorter than what’s typically required to achieve your goals, that old way of approaching portfolio construction needs a bit of refinement.

But before that, some general strategies on how I think about portfolios. I follow a core and explore approach to portfolio construction where the vast majority of my family savings forms the core with the remaining and a very tiny portion at the margins forming the explore. The core is what’s going to take care of my family’s income needs when we need it. The explore will either knock the ball out of the park or will strike out. Don’t care. But for you, unless you have a solid core, there is no reason to do explore. I do it because I am at a point where the absence of explore is not going to change anything in my family’s life. This explore also fulfills some of the alternative investment bucket option within my overall family’s financial plan.

What’s in explore will trickle in here and there from time to time but the core is what I will address here. The global market portfolio excluding hard assets is about 50% stocks and 50% bonds. That is what we all own collectively on this planet. So that becomes our baseline. Now depending upon where you are in life, you might have to adjust that stock-bond mix to get to a ratio that is just right for you at a given time. Setting aside discussion on bonds for now, the stock component of the global market portfolio as it stands today is split almost evenly between U.S. and international (ex-U.S.). Now since I live in U.S., spend my money in U.S. and will likely retire in U.S., I need to design in a U.S. tilt to my portfolio. Some call it a home country bias though tilt is a much milder form of home country bias but that again depends upon where I am going to spend my money…eventually. But once I have the U.S. vs. international proportions defined, I can start getting into the nuts and bolts of what to populate my portfolio with.

To do that, from time to time, I compile datasets of portfolio holdings from a variety of investment providers that allows me to dig deep to assess what each of them have to offer. So I use a lot of copy / paste in bringing that data into Excel 😉 but you can use any tool of your choice that hopefully allows you to automate this drudgery.

So back to this, a few thoughts on populating the U.S.-centric component of my portfolio. The easiest way to get that exposure is to buy the entire U.S. stock market in one fell swoop. I like the index compiled by the Center for Research in Security Prices (CRSP) for its completeness and which Vanguard has adopted so I’ll use that dataset to point out a few things.

- You buy this and you buy stakes in 3,618 U.S.-based companies as of this writing.

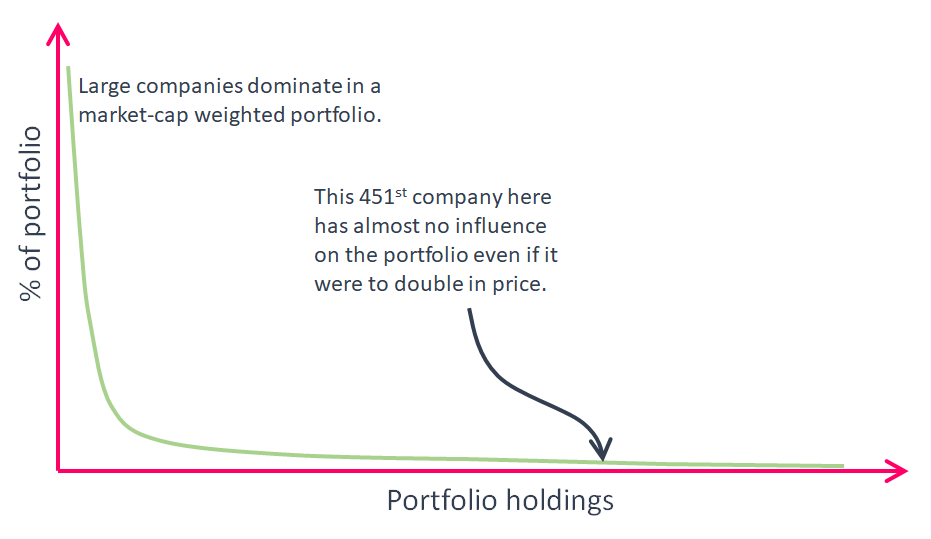

- The top 10 companies use up 17.8% of your money in this investment.

- The top 50 companies occupy 42% of your money and the top 100 companies, 55%.

- The bottom 3,518 companies take the remaining 45%.

The other popular investment that most of us are familiar with is the S&P 500 index. You buy this and you get to own 500 of the biggest companies in the U.S. because it is after all a large-cap index. Cap by the way is short for market capitalization, the market value of a company.

But S&P 500 faces the same set of issues as the total market index described before does where the ownership is very top-heavy with only a small fraction of your dollars going to mid and small-size companies.

So what’s wrong with a top-heavy investment portfolio? If you believe in pure meritocracy, nothing. The top companies got to where they are because they evolved to dominate their industries, crushing their competition along the way. Or they created something totally new that changed the way we live and the market rewarded them for that.

But there probably was a natural progression for most of these companies from small upstarts to becoming mid-size and then becoming the top dog. So if you buy only this one investment, you miss that transition and the associated growth from small to mid and from mid to a large company.

Plus being so top heavy has its own set of risks as any dislocation in one or two of the companies at the top can have an outsize impact on your portfolio. And I have a personal bias against how some of these top companies are run because I’ve dealt with many of them in one setting or the other. They become too big, too lethargic, too bureaucratic and are an easy prey to nimble upstarts. So capitalism and its forces of creative destruction will replace these companies that are at the top today with companies of tomorrow and you want to participate in that process.

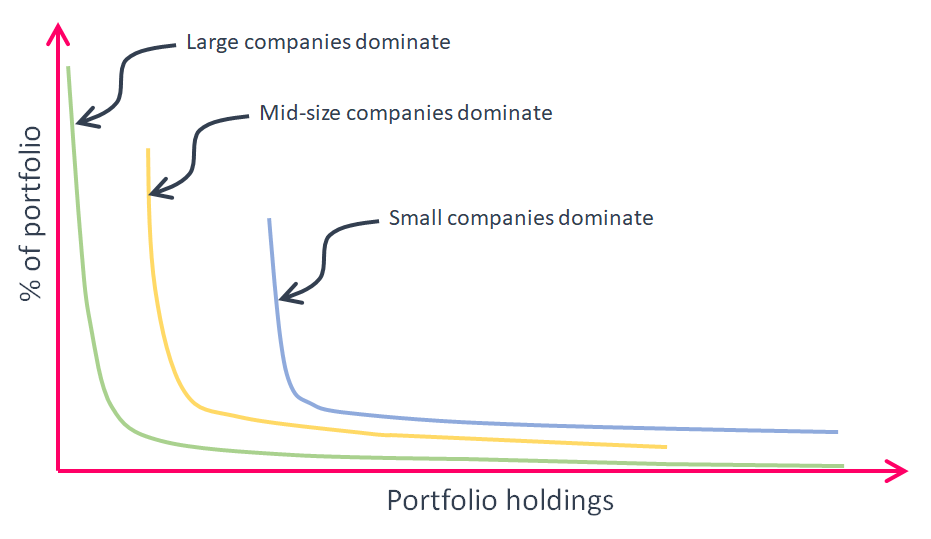

So then you start to look beyond the investments that are large-cap heavy to get exposure to mid-size and smaller companies for an ‘optimized’ portfolio blend.

To get to that, I go back to using the CRSP indices again that target these market segments. There is a third type of investment that I use to get exposure to small/mid-size companies through an extended market or the completion index. The extended market portfolio comprises of all the companies that are found in the total stock market index but without the companies in S&P 500.

A few things I found that I feel you’ve got to know if you care to know 🙂 .

- All companies found in S&P 500 are also found in the total market index. That’s expected so no big surprise there. But when you buy only total market index, 83% of your money goes to companies in S&P 500 with only 17% devoted to small and mid-size companies.

- Companies in the extended market index and the S&P 500 index are almost 100% mutually exclusive. Knew that but wanted to verify. So if you own one index, you completely exclude the companies from the other index. If you own CRSP total market index, you own both though not in the same proportion so your exposure to small and mid-size companies is limited.

- The overlap between mid-cap and small-cap CRSP portfolios is negligible with only 26 companies that are common to both indices. 3% of your money in a mid-cap portfolio overlaps with holdings in small-cap whereas 2.7% of your money in small-cap overlaps with holdings in mid-cap. So both of these are almost mutually exclusive.

- Out of the 366 holdings in the mid-cap index, 256 of them are already present in S&P 500 so that’s a pretty big overlap. In % terms though, if you own S&P 500, only 14.5% of your money is invested in companies that belong to the mid-cap index. But if you own the mid-cap index, 78% of your money goes to companies that are also found in the S&P 500 index though the proportion of your dollars to mid-size companies is quite a bit larger. So if you want to balance out your portfolio exposure to more nimble yet financially stable companies, you’ve got to have exposure to mid-cap companies. This helps spread out your dollars across a broader set of companies than just the large-caps.

- There are 3,288 companies in the completion index though only 111 could be found in the CRSP mid-cap portfolio. This makes sense as a lot of the companies in the mid-cap portfolio are also found in S&P 500 and none of the S&P 500 companies are found in the completion index. In percentage terms, if you buy the completion index thinking that you are buying exposure to the mid-cap space of the U.S. stock market, you might want to rethink that because only 20% of your money in this investment gets you that mid-cap exposure. On the flip side, if you buy the mid-cap portfolio, only 23% of your dollars are invested in companies that are found in the completion index. Plus oftentimes, you miss exposure to quite a few fast-growing and prominent companies if you decide to buy one or the other.

- So what’s in the completion index then? But before that, a bit about the CRSP small-cap index. There are a total of 1,408 companies in that index out of which 1,373 can also be found in the completion index. So the completion index which is usually thought off as a mid + small-cap index is truly a small-cap index. In % terms, if you own the completion index, 70% of your money goes to companies that are already in the small-cap index so if you own both, you have an outsize exposure to smaller names and not much to mid-size companies. If you own the small-cap index instead, almost 96% of your money goes to companies that are also in the completion index. So when and where if I have access to the completion or the extended market index, I buy that instead of the small-cap portfolio. Plus you get exposure to 1,821 more companies in the completion index that are not found in either the small or mid-cap indices. In % terms, that’s 12.6% of your money in the completion index that goes to companies that are not in either of the two indices.

So that covers the domestic front, on to international…

The easiest way to populate the international bucket is to buy the entire basket of international stocks in one shot through an investment that tracks the FTSE global all cap ex-US index. You buy that and you pretty much own all publicly traded companies in every country outside the United States. This is not as egregiously top-heavy as what you can find with the total U.S. stock market tracker but it has the same type of over-concentration at the top issues. A few stats about this particular investment…

- You buy this and you own stakes in 6,372 companies outside U.S. spanning almost every country around the world.

- The top 10 companies use up 8% of your investment dollars.

- The top 50 companies occupy 22% of your international stock portfolio and the top 100 companies, 32%.

- The bottom 6,272 companies take up the remaining 68%.

To optimize further and to get exposure to potentially more volatile yet faster growing companies, I split this one investment into two parts –

- FTSE all-world ex-U.S. portfolio that provides me exposure to larger, more established companies, 2,761 in total.

- FTSE global small cap ex-U.S. portfolio with exposure to 3,612 small and mid-size companies.

To increase tilt in favor of faster growing emerging markets, I add a third element to this mix of international stocks through an FTSE emerging markets all-cap portfolio.

Here are my findings when I dug deep into the holdings of these four different investment options…

- Pretty much everything in FTSE all-world ex-U.S. and FTSE global small-cap ex-U.S. portfolios is already in FTSE global all-cap ex-US index.

- Only 10% of my money goes to smaller-cap international companies when I buy FTSE global all-cap ex-US index. The remaining 90% of my money then is invested in companies that are found in FTSE all-world ex-U.S. portfolio (its large-cap brethren).

- There is almost no overlap between FTSE all-world ex-U.S. portfolio and FTSE global small cap ex-U.S. portfolio. That helps me to increase exposure to smaller companies if I need to by increasing allocation to the latter.

- Out of the 4,616 companies in FTSE emerging markets all-cap portfolio, 1,115 can be found in FTSE all-world ex-U.S. portfolio and 1,165 in FTSE global small-cap ex-U.S. portfolio. Add the two and about that is what you find in FTSE global all-cap ex-US index from the emerging markets angle. That leaves about 2,336 companies that I don’t have exposure to if I were not to include the emerging market segment in my portfolio.

- About 20% of my dollars are devoted to emerging market stocks in FTSE global all-cap ex-US, FTSE all-world ex-U.S. and FTSE global small cap ex-U.S. portfolios. The remainder in all three is exposed to companies in the developed world outside the United States. That allocation is quite right but I tend to employ a slight tilt in favor of emerging market economies and hence this added option.

- 87% of my money in FTSE emerging markets all-cap portfolio is invested in companies that are also found in FTSE all-world ex-U.S. portfolio, 8.5% of it is invested in companies within FTSE global small cap ex-U.S. portfolio and the remaining 4.5% is invested in companies that are only found in the emerging market segment. That as mentioned before, is invested in the 2,336 companies that are exclusive to the emerging market component of the total portfolio.

So there, some general thoughts on portfolio design. I have intentionally not listed specifics on what I own and in what proportions because every situation is different. Plus these portfolios and proportions evolve over time along with changes in the markets and your goals so its applicability is likely different for everyone. Though I tend to think that this is it, the task is never really, really done because in the words of Salvador Dali, perfection will always remain elusive.

Have no fear of perfection – you’ll never reach it.

But I’ll keep trying.

Until later.

Cover image credit – Bruin, Flickr