Erin Botsford in her book, The Big Retirement Risk says that buying bonds in the wrong market environment could be as dangerous as buying Florida condos in 2005.

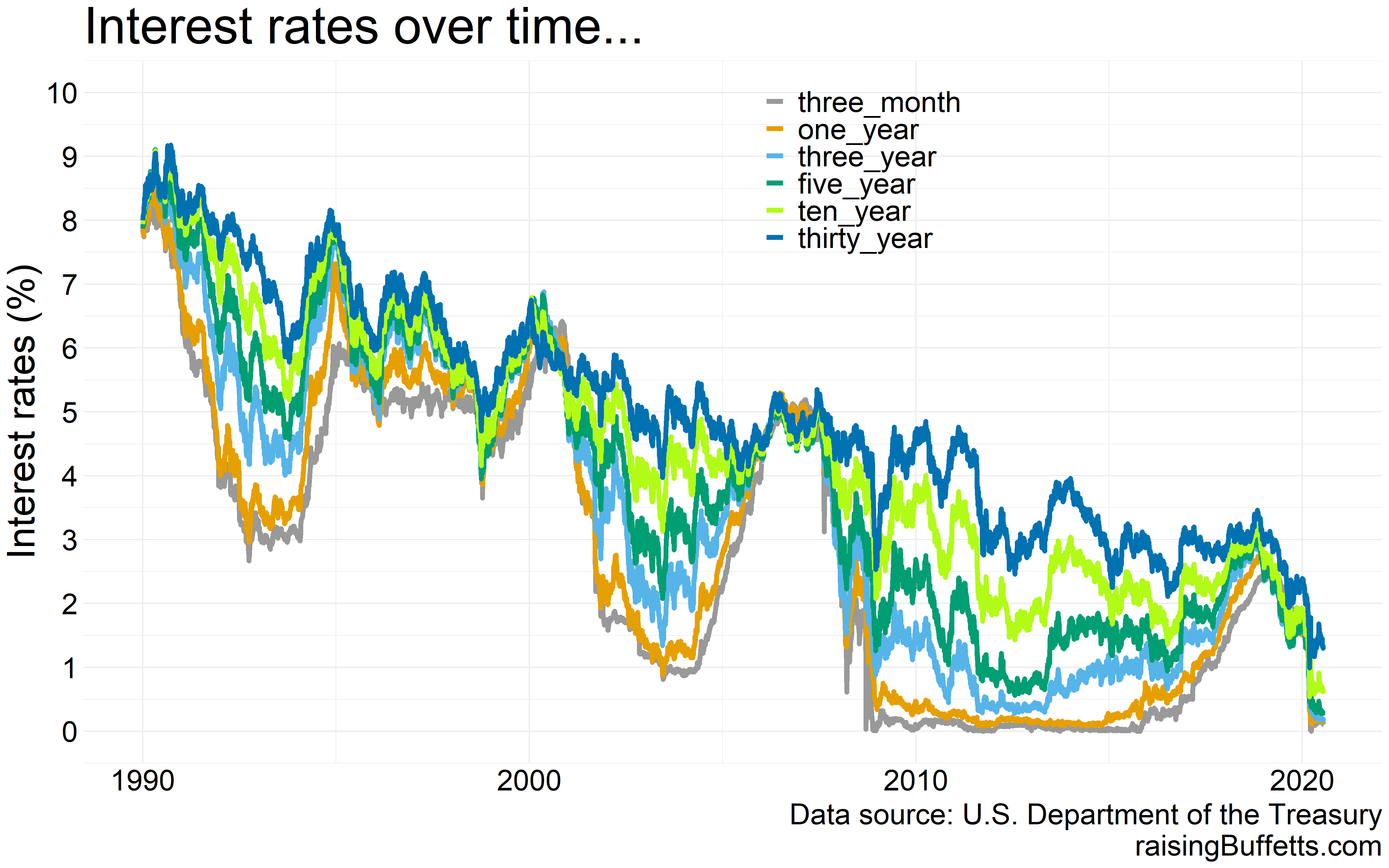

So what’s a wrong market environment? This…

Are you seriously telling me that people are willing to lend money today to the U.S. government for 30 looooong years to earn a puny, pathetic 1.3% a year for that entire duration? What does that tell us about the state of our economy and our future? Nothing good as such.

That grey curve by the way, literally hugging the floor for close to a decade, that’s what the Federal Reserve had to do to keep the economy afloat in light of the banking crisis of 2008. And short duration rates are the only rates the Fed or the European Central Bank and other Central Banks around the world control. The longer term rates are decided by the markets. If investors in aggregate expect that the lowering of rates by the Central Banks will ignite inflation out in the future, they will expect to be paid for taking on that risk. And hence, longer-term rates are usually always higher than the shorter-term ones.

But before all of that, a bond as we all know represents a loan an investor makes to an entity. That entity could be the U.S. government, a local municipality, a corporation or a foreign country. They need money and you have money so you lend it out at an agreed upon interest rate that the market decides.

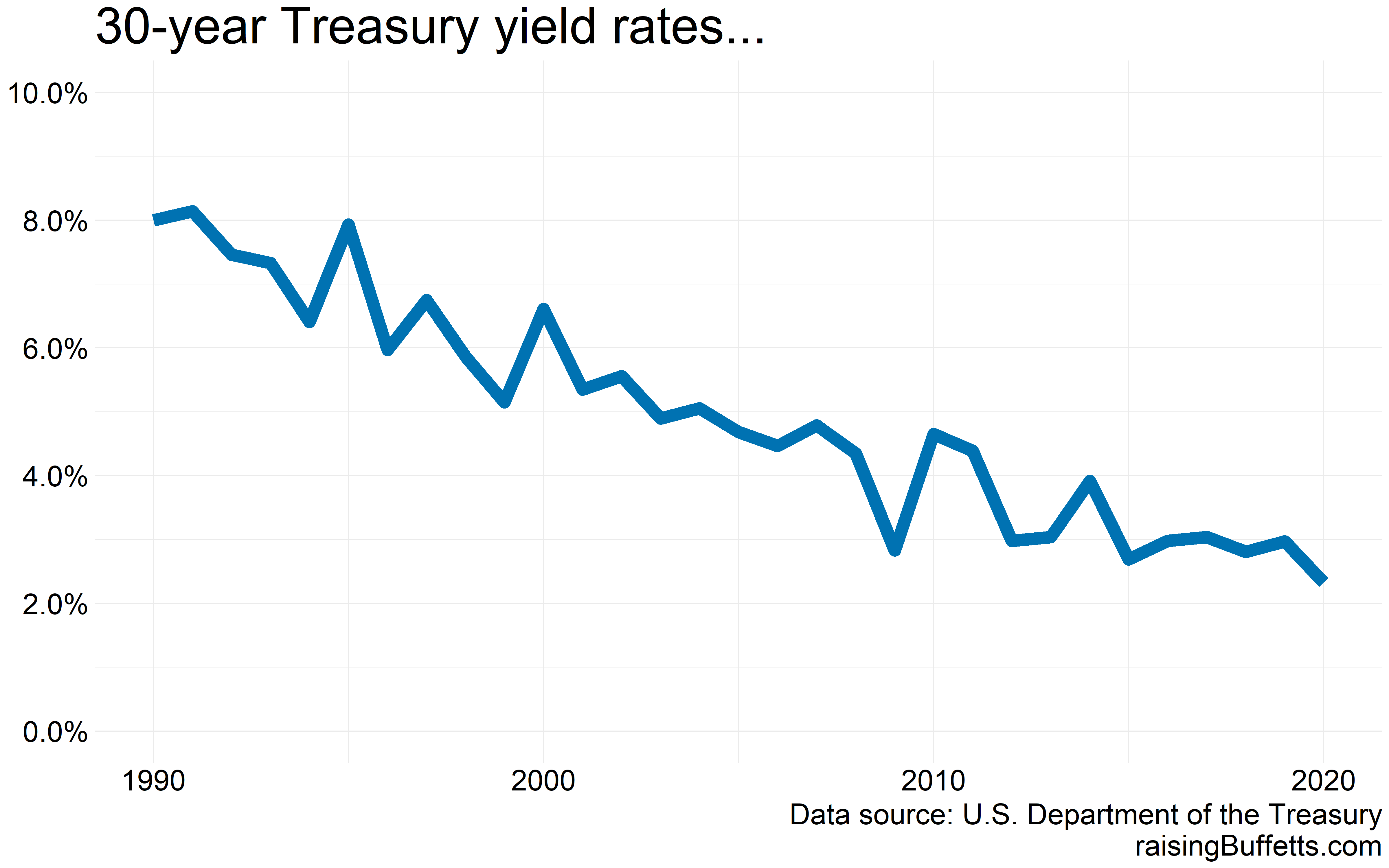

And interest rates and bond prices move in the opposite direction. As interest rates rise, bond prices fall and vice-versa. So say you buy a 30-year bond today yielding 1.3%. If you hold that till maturity (for all of 30 years), you will get that yield every year and at the end of that term, you’ll get your principal back.

But say rates rise to 3% next year and for some reason, you decide to sell that bond. Would you be able to sell at the same price you bought it at? Hell no. You will have to discount that bond to a price that equates to what the market yields are. So you’ll take a hit on a supposedly safe investment.

The lower the rates and the longer the duration, the harder the price falls when interest rates rise. So if you are buying a bond with a duration longer than say 5 years, expect a lot of volatility if interest rates change.

You add bonds to a portfolio to dampen the overall volatility of a portfolio and if that is the intent, short-duration bonds are your only choice now. Short-duration bonds yield zilch today and hence any portfolio that includes them in a proportion that was historically deemed reasonable will not return as much. And that’s the reality.

But don’t show that light to the many city and state pension funds that are still assuming a 7% rate of return in their calculations. And even with that, they are so deep underwater that bailouts would be the only recourse. Or a significant haircut in what as a pensioner you should expect. So it’s best to plan for it and don’t assume that the income that’s promised will be there for you when you need it.

So what are some of the other implications of the interest rate predicament we find ourselves in? For one, it inflates prices of everything around us. Take for example that rental property you were exploring a few years back. You might have been balking at the 8% net yield thinking it was low.

But then the interest rates cratered and suddenly you are on board even at a 5% yield. How did the yield get to 5%? The price of that property rose. Or maybe the landlord marked down the rents. Ha…

Or say that iffy investment you were trying to make in your business just a few short years back. It doesn’t look as iffy anymore. You will gladly pursue that high risk, low reward deal because the hurdle rate is so damn low.

Or take stock market valuations for example. I hate to pick on Apple but let’s use that as a way to prove a point. It’s a 1.7 trillion dollar market value company that trades at a price to earnings multiple of 30. That’s an earnings yield of 3.33% for a company that did $260 billion in revenue last year.

But that yield is not that far away from what a 30-year bond yields today. Granted, the bond will never yield more than the stated yield but a business can for sure grow its revenues and profits. And that is the expectation.

Buying a stock in a sense is like buying a bond but without a maturity date. It basically is an annuity that pays indefinitely (perpetuity) because businesses in theory can last forever. But they don’t and we all know that. Someday, even the mighty Apple will not be Apple and will be replaced by something new. And history is replete with that scenario panning out.

Investors are willing to pay that much more for a company that size is because of something called TINA (there is no alternative).

But then Apple is a cash generating powerhouse so maybe it deserves that valuation. Time will tell. But the rest of the market and especially with tech has completely gone off the rails. I am not saying a crash is imminent because there is a theoretical backstop to that with all this liquidity being pumped into the system. That money has to go somewhere.

But it should not come as a shock to anyone if there is one because the fact that you have money in your pocket does not mean you pay whatever you want for an asset. Fundamentals rule, eventually.

And there is one place this interest rate situation impacts all of us and that is with housing. The interest rates first…

Your mortgage of course will be at a rate a percent or two higher than what the Treasuries yield (imagine a 10% mortgage rate back in the 1990s…) but let’s just go with this.

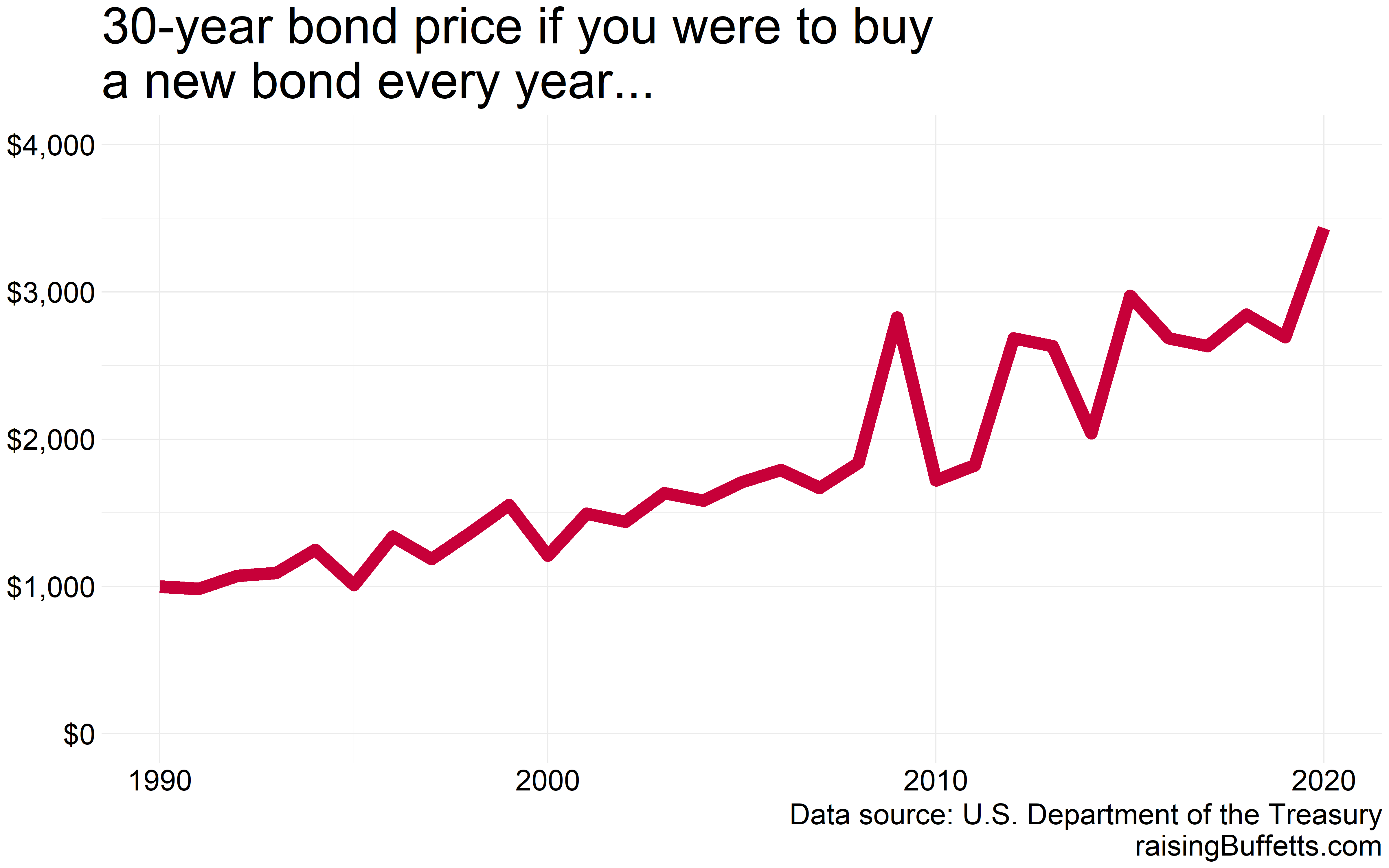

And since bond prices rise if and when rates fall, this is the corresponding rise in the price of a 30-year bond over time…

So if you bought a home in 1990, the value of that asset quadrupled just because the rates dropped and dropped and dropped, all other factors remaining constant of course.

So you have about the same risk of buying a home now as you have with any long-term bond.

But then a home is where a heart is and if it was not a quality of life ONLY decision in the past, it better be one now. Because that interest rate magic is going to work against you if and when rates turn, all other factors remaining constant again of course.

So that’s about it. Thank you for reading.

Until later.

Cover image credit – Cottonbro, Pexels